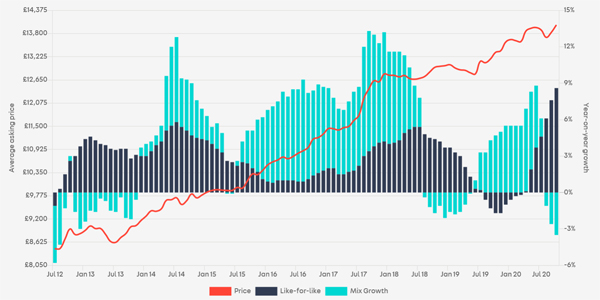

Prices have been driven by both supply constraints in the market, and the strong levels of consumer demand, which despite the various lockdowns and restrictions imposed across the UK in 2020, remained robust throughout the year. On Auto Trader, 2020 saw over 673 million visits to its marketplace, which is an 11% increase on 2019, and in December alone, visits increased 20% YoY.

Whilst traffic eased during the run up to Christmas, it accelerated dramatically shortly there afterwards and into the new year. In fact, during 27th December – 3rd January, visits and advert views grew 30% and 33% respectively when compared with the festive period (24th – 26th December). This increased level of engagement resulted in a 65% growth in the number of leads being sent to retailers during the same time periods. During the first full week of the new year (4th – 10th January), there was a daily average of 1.8 million visits to Auto Trader, which was flat (0.1%) against the same period last year.

Retailers holding firm

Testament to their confidence in the market, the number of retailers making price changes and the value of those price adjustments made in December remain lower than pre-COVID levels. 1,937 retailers made price changes last month, which was 4.2% fewer than in December 2019, whilst the average daily reduction was £262: -7.6% less than the same time last year. The average number of cars being changed each day was 13,082, which is far fewer than the 17,500 to 24,000 typically adjusted during normal trading conditions.

Commenting on the results, Auto Trader’s director of data and insight, Richard Walker, said:

“Encouragingly, we can see that the tighter restrictions rolled out across the UK throughout December had little impact on the levels of consumer demand. Whilst sales capabilities were limited to click & collect and home delivery, we saw millions of consumers visiting our marketplace and engaging with our retailer partners, which suggests there was a healthy market available. Early signs suggest that January consumer demand will remain robust, despite the recent increase in restrictions.

“Consumer demand, along with constrained supply, is sustaining price growth, so, far from requiring a big correction in pricing, with such strong engagement we have every reason for optimism that prices will remain strong in Q1. As with the previous lockdowns, we strongly urge retailers to trust the data and continue to hold firm with their prices, which as we saw throughout 2020 helped ensure retailers achieved much stronger margins than if prices were adjusted unnecessarily.”

Electric appetite surges as ICE demand cools

Looking at the pricing data at a more granular level, we can see the influence of supply and demand dynamics on the market. Demand for petrol increased 0.6% YoY in December, whilst the levels of supply grew 3.5%. This minor imbalance, in favour of supply, contributed to the slight easing in the rate of price growth for used petrol cars, slowing from 8.8% YoY in November to a still very high 8.1% last month. The average sticker price was £12,751.

The rate of growth for used diesel prices also saw an easing, albeit a marginal one, slowing from a record 9.2% in November to 9.0% last month, with an average price of £14,741. Demand for diesel however fell, down -7.7% YoY, whilst levels of supply fell even further, dropping -13%.

In contrast, electric vehicles (EV) continue to record exceptionally strong levels of demand. Premium EVs saw demand increase 80.8% YoY in December. However, with a much stronger level of supply in the market, which was up 223.9%, prices contracted slightly, decreasing -1.70% YoY (£46,432). Whilst demand for volume EVs was slightly lower, up 58.7% YoY, the gap between levels of supply was far smaller, at 86.9%, helping to drive average prices up 16.20% (£19,197).